Codat

成立一年

2017年阶段

C系列 |活着总了

166.52美元估值

0000美元最后提出了

100美元 | 10 mos前马赛克的分数

马赛克评分是一种算法,私营企业的整体财务状况和市场潜力。

+ 10分在过去的30天

esp包含Codat

ESP矩阵利用数据和分析识别和了解排名领先的公司在一个给定的技术格局。

贷款的基础设施提供商帮助企业构建端到端的数字贷款解决方案使用应用编程接口(API)。这些接口促进数字平台之间的数据传输和贷款发放银行数据库和维修。例如,格子的放贷API允许银行轻松访问customer-permitted银行工资和资产数据做出lendin…

与Codat吗?

确保你的公司和产品准确地代表在我们的平台上。

Codat的产品和优势

机载、决策和监督

Codat的机载、决策和监控应用程序变换的过程评估为SMB提供金融服务的风险。他们让我们的客户和顾客安全分享实时、全面的数据直接从客户的计费程序包,商务平台,和银行。他们提供这些数据的标准化和正常化格式可以被映射到我们客户的现有的模板和流程。

研究包含Codat

获得CB的数据驱动的专家分析见解信息部。德赢体育vwin官方网站

德赢体育vwin官方网站情报分析家提到Codat CB见解1 德赢体育vwin官方网站CB见解研究短暂,最近在2022年6月6日。

2022年6月6日

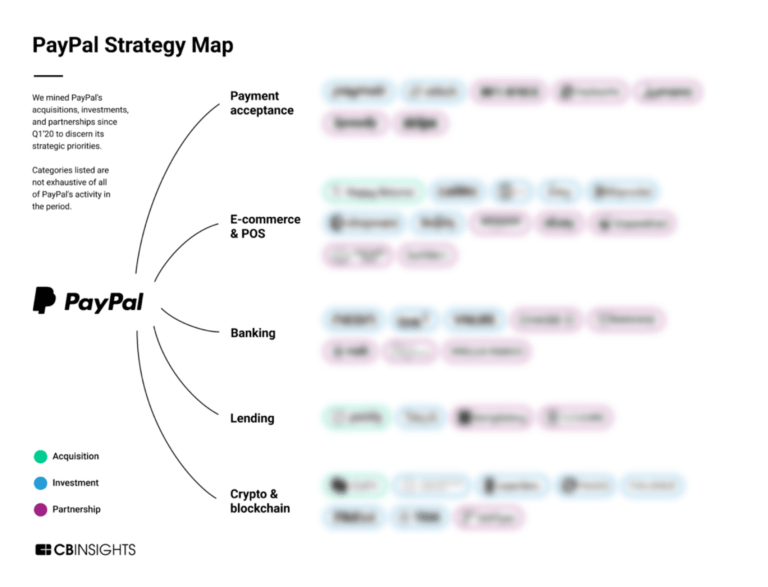

分析贝宝的增长战略:支付巨头是如何扩大超出付款专家集合包含Codat

专家集合是analyst-curated列表,突出了公司你需要知道的最重要的技术空间。

Codat包含在6专家集合,包括银行。

银行

1221件

数字的贷款

1985件

这个集合包含公司提供替代方法获得贷款用于个人或商业银行为应用程序提供软件的公司,承销、资助或贷款收集过程。

SMB Fintech

1230件

支付

2680件

公司和初创公司在这个集合使消费者、企业和政府支付对方——在线和在物理销售点。

Fintech 250

499件

250年的顶级fintech公司将金融服务

Fintech

5141件

跟踪和获取公司信息和工作流。

最新的Codat新闻

2023年3月24日,

现在3分钟读寄存器左起:Ambika沙玛,创造者的Fintech咖啡馆,Kareem萨利赫,公平竞赛的创始人兼首席执行官,戴夫•霍尔的共同创始人兼首席技术官,Codat, Seshu Guddanti,高级副总裁和高级软件工程主管服务器消息块平台对美国银行和约翰·戈登,呱呱的首席运营官。弗兰克加银行和信用合作社正越来越多地使用替代消费信贷数据,如银行账户信息,加强项目“重新审视融资”和贷款进入的市场。最近LexisNexis风险解决方案的调查大约225高级决策者营销、金融机构贷款和信用风险在美国发现,65%的受访者使用替代信贷数据增长50%到100%的所有新的申请者。因此,超过一半的营收增加15%,更高。U.S. Bancorp在辛辛那提是使用替代数据为小企业客户开发一个全面的银行平台,组织客户的账户和编译所有的收入和资产报表用于一个仪表板。在某些情况下,申请人的历史作为一个消费者可以填补空白的信用记录作为一个企业经营者,例如。Seshu Guddanti、高级副总裁和高级软件工程主管服务器消息块585美元billion-asset银行平台,解释如何应用平台的心态总消费账户和性能数据可以帮助银行提供更多的产品和服务。他强调,不限制客户的数据被归类为小企业客户,“也可能是一个消费者,也可能是一个抵押贷款的客户。…所以我们认为一旦这个数据聚合的平台,它可以使用许多不同的团队在银行对这些数据做出自己的决定,”Guddanti说在一个小组讨论Fintech Meetup本周早些时候在拉斯维加斯举行的会议。替代数据也帮助银行实现欠发达市场。 Companies that solely use data from credit agencies can unfairly perpetuate biases towards underserved communities and further the divide between them and lenders, said Kareem Saleh, founder and chief executive of the Los Angeles-based fairness solutions firm FairPlay . "It turns out that, especially if you're building models on credit bureau data, that the data is kind of overfit to the majority population. …[This] means that there are these subpopulations [of consumers] that are not well represented in the data whose riskiness can be overstated," Saleh said. As an alternative to traditional metrics, companies like Ribbit, a data solutions provider based in Oxford, Ohio, are helping financial services firms develop models for lending by analyzing consumer-provided account data and non-credentialed data to build a more comprehensive credit profile. In the case of firms that engage in second-look financing — which are loans offered to consumers whose credit scores generally fall below 680 and are turned away by larger institutions — the established rating methods are oftentimes not enough by themselves to render a confident decision, said John Gordon, chief operating officer for Ribbit. "For us, we believe that the [consumer's bank account] offers the clearest window into that consumer's financial health as well as ultimately what they can afford, so that you're creating the best possible relationship" between the financial institution and the consumer, Gordon said. Many small-business owners just starting out are facing a similar challenge when applying for lines of credit due to relatively incomplete performance profiles with rating agencies such as Equifax and Experian — leaving entrepreneurs with few options for funding and lenders with the question of how to best determine their credit worthiness. Dave Hoare, chief technology officer and cofounder of the London-based application programming interface firm Codat , explained how lenders integrated into a business client's point of sale system can obtain real-time transaction data to use as an up-to-date resource for assessing the creditworthiness of an applicant. "They can see sales literally up to the minute, they can see which products are selling well, they can see how sales have gone up over the months, they can see payment information and they just have this sort of closer-to-the-bone view of how the business is operating, rather than purely depending on [outdated] bureau data," Hoare said.

Codat常见问题(FAQ)

Codat是何时成立的?

Codat成立于2017年。

Codat总部在哪里?

Codat总部位于301墨水房间,伦敦。

Codat的最新一轮融资是什么?

Codat系列的最新一轮融资是C。

Codat筹集了多少钱?

Codat筹集了总计166.52美元。

Codat的投资者是谁?

Codat的投资者包括指数投资,贝宝公司,格子,Shopify Canapi企业6更多。

Codat的竞争对手是谁?

Codat的竞争对手包括合并、Railz DemystData upSWOT Weav和12。

Codat提供什么产品?

Codat的产品包括车载、决策和监控和3。

Codat的客户是谁?

客户Codat包括Zettle、ClearCo烟斗,总结和Capchase。

比较Codat竞争对手

upSWOT帮助中小企业成长和做出更好的财务决策。公司部署的白标签业务财务管理解决方案与金融机构合作,upSWOT总量从会计和分析数据,人力资源、ERP、电子商务和其他SaaS系统常用的中小型企业。它成立于2019年,总部位于夏洛特,北卡罗莱纳。

ForwardAI是一个贷款商first API技术最强劲的会计和财务数据套件提供小型企业贷款。

Railz提供了一个单一的应用程序编程接口(API)会计软件服务提供商。它支持按需访问金融交易,分析见解和报告。它成立于2020年,总部设在多伦多,加拿大。

老板的见解提供了一个数据平台数字化贷款发展业务关系。它赋予债权人增加个性化的销售机会,加快从月分钟并提供银行商业贷款,信用合作社,以及私人银行与实时了解他们的商业客户。公司成立于2017年,总部设在多伦多,加拿大。

Enfuce提供支付和银行服务银行开放,fintech公司,金融运营商,和商人。通过结合行业专业知识,技术,和遵从性,该公司提供长期、可伸缩的解决方案,快速和安全。

Monit是个聪明的财务现金流分析,预测和指导平台。会计软件包的链接的中小型企业(smb)和提供清晰的视图当前和预测现金流,收入和盈利能力。公司成立于2019年,总部设在李约瑟,马萨诸塞州。

发现正确的解决方案为您的团队

CB见解德赢体育vwin官方网站科技市场情报平台分析数百万数据点在供应商、产品、合作关系,专利来帮助您的团队发现他们的下一个技术解决方案。